Market Updates

Share

Stocks Trade Higher on Strong Q2 Earnings & Trade Deals

By STEPHEN T. HART, CFP®

08/01/2025

Monthly Market Summary

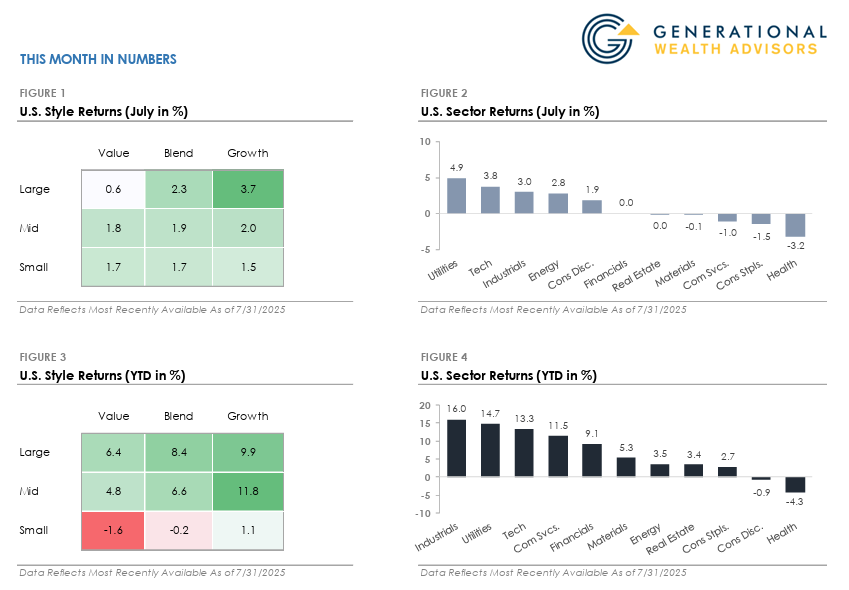

- The S&P 500 Index rose +2.3% in July, pushing its year-to-date return to +8.4%. Large Cap Growth stocks led with a +3.7% gain, while Large Cap Value gained +0.6%.

- Utilities was the top-performing sector, with the Technology, Industrials, and Energy sectors also outperforming the S&P 500. Defensive sectors underperformed, with Health Care, Consumer Staples, and Communication Services all trading lower.

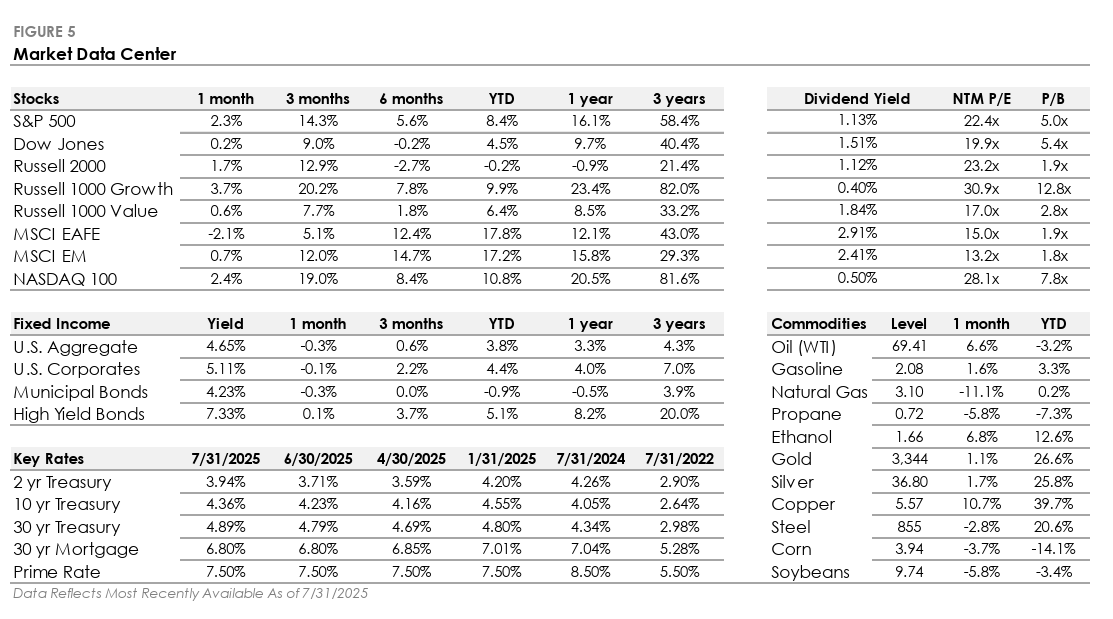

- Bonds posted a modest loss as Treasury yields rose. The U.S. Bond Aggregate returned -0.3%, with longer maturity Treasury bonds underperforming the index. Corporate bonds outperformed as credit spreads tightened, with investment-grade posting a -0.1% total return and high-yield gaining +0.1%.

- International stocks underperformed the S&P 500 as the U.S. dollar strengthened. Developed Markets fell -2.1%, while Emerging Markets returned +0.7%.

Strong Q2 Earnings & Trade Agreements Send Stocks to All-Time Highs

Stocks climbed to new highs in July, with the S&P 500 and Nasdaq both logging six consecutive record closes late in the month. Investor sentiment improved after betterthan-expected Q2 earnings and trade agreements with Japan and the EU, with tariff rates on the deals less severe than feared. Market breadth improved early in the month as smaller companies outperformed the S&P 500. However, by month-end, market leadership was top heavy again, with the Magnificent 7 gaining over +5% after leading AI firms reported strong Q2 earnings. Volatility remained subdued for most of July, and the VIX fell below 15, signaling investor confidence but hinting at potential complacency.

Stock valuations are stretched after the multi-month rally from April’s lows. The S&P 500 trades at over 22x its next 12-month earnings, up from around 18x in early April and well above the 16.8x average since 2000. Today’s extended valuations mean the market is more reliant on earnings growth to fuel gains, which gives companies less room to disappoint. Although the tariff rates in recent deals were lower than feared, the overall effective tariff rate has risen sharply this year. The higher effective tariff rate raises questions about the long-term impact on corporate earnings, consumer demand, and economic growth, as well as the potential near-term impact on inflation.

Interest Rate Cuts Continue to Be Pushed into the Future

After cutting interest rates by a full percentage point in late 2024, the Fed has held interest rates steady through five meetings this year. The pause in the Fed’s rate-cutting cycle reflects two dynamics: inflation progress has stalled, with core CPI stuck near 3.0%, and the labor market remains solid, with unemployment holding near 4%. Policymakers are concerned that tariffs could reignite inflation, and they’ve consistently emphasized the need for patience while they wait for more clarity in the data.

From a markets perspective, rate cut expectations have been on a rollercoaster. Earlier in the year, an anticipated March cut was delayed to May, then to June, and ultimately to September. Following the July FOMC meeting, odds of a September cut dipped below 50%, with markets tentatively shifting expectations to October and pricing in just one cut for the year.

However, that has changed swiftly. A weaker-than-expected July jobs report and rising concerns about economic softness have pushed the probability of a September cut above 85%, with some measures placing it as high as 94%. Markets are now pricing in two cuts by year-end, reversing the prior view that the Fed might stay on hold. The takeaway: with mixed signals from both data and Fed communications, the market remains reactive—pricing policy one meeting at a time, but currently leaning dovish.

Important Disclosures

Generational Wealth Advisors (“GWA”) is an SEC registered investment adviser. Information presented is for educational purposes only and is intended for a broad audience. The information does not intend to make an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies. Investments involve risk and are not guaranteed. GWA has reasonable belief that this information does not include any false or materially misleading statements or omissions of facts regarding services, investment, or client experiences and that the content as a whole will not cause an untrue or misleading implication regarding the adviser’s services, investments, or client experiences. GWA has reasonable belief that the information is presented in a fair and balanced manner. GWA does not provide tax, legal, or accounting advice. Consult a professional tax or legal representative if needed.

The information and opinions provided herein are provided as general market commentary only and are subject to change at any time without notice. This commentary may contain forward-looking statements that are subject to various risks and uncertainties. None of the events or outcomes mentioned here may come to pass, and actual results may differ materially from those expressed or implied in these statements. No mention of a particular security, index, or other instrument in this report constitutes a recommendation to buy, sell, or hold that or any other security, nor does it constitute an opinion on the suitability of any security or index. The report is strictly an informational publication and has been prepared without regard to the particular investments and circumstances of the recipient.

Past performance does not guarantee or indicate future results. Any index performance mentioned is for illustrative purposes only and does not reflect any management fees, transaction costs, or expenses. Indexes are unmanaged, and one cannot invest directly in an index. Index performance does not represent the actual performance that would be achieved by investing in a fund.